Networking as Competitive Infrastructure in Asia

Executive Takeaways

Asia’s trade growth is increasingly intra-regional, powered by dense production networks and agreements such as RCEP — not simply export expansion.

In FMCG and consumer sectors, network strength determines regulatory speed, distribution depth, cost efficiency, and resilience.

Leaders expanding into Asia must treat networking as strategic infrastructure — auditing legacy partnerships and aligning with evolving trade corridors and digital channels.

Why This Matters for International Expansion

Asia’s international trade system is no longer defined solely by scale.

It is defined by connectivity.

Over the past two decades, trade volumes across the Asia-Pacific have expanded significantly, supported by tariff reductions, shared trade rules, and trade facilitation policies. The China–Southeast Asia corridor alone reached approximately USD 468.8 billion in trade in 2023, reinforcing the region’s structural integration.

Production-sharing processes have densified across borders. China operates as a central assembly and distribution hub, while ASEAN economies increasingly function as specialized manufacturing pivots. Unlike other regions where political agreements drive integration, East Asia’s interdependence has largely been built from industrial relationships upward.

Market fundamentals remain compelling:

Asia’s FMCG market grew 3.5% in early 2024

Beverage sales increased by 9.2% in value terms

Rising single-person households in South Korea and expanding middle classes across Southeast Asia are reshaping packaging, pricing, and channel expectations

Spending per shopping trip has risen in China and India despite cautious macro conditions

Digital transformation is accelerating these shifts. E-commerce penetration is rising. Logistics networks are expanding. Cross-border infrastructure is improving.

In this environment, networking is not about introductions or conference relationships.

It determines:

Speed of regulatory alignment

Access to multi-channel distribution ecosystems

Optimization of trade agreements

Supply chain resilience

Real-time consumer intelligence

Expansion in Asia is therefore not simply a market selection exercise.

It is an ecosystem integration decision.

Where Leaders Miscalculate

The most common strategic error is assuming that capital and product strength alone guarantee success.

Leaders often underestimate:

Variation in market maturity across Asia

Cultural and diplomatic influences on trade dynamics

Regulatory complexity and FTA optimization requirements

The speed at which consumer channels evolve

Insufficient network depth leads to:

Limited market intelligence

Higher transaction costs

Regulatory delays

Vulnerability to entrenched local competitors

Slower innovation cycles

An even subtler mistake is overreliance on legacy networks.

Long-standing partners provide trust.

They do not automatically provide digital capability, diversified corridor exposure, or regulatory agility.

Historical relationships must be reassessed against current strategic requirements.

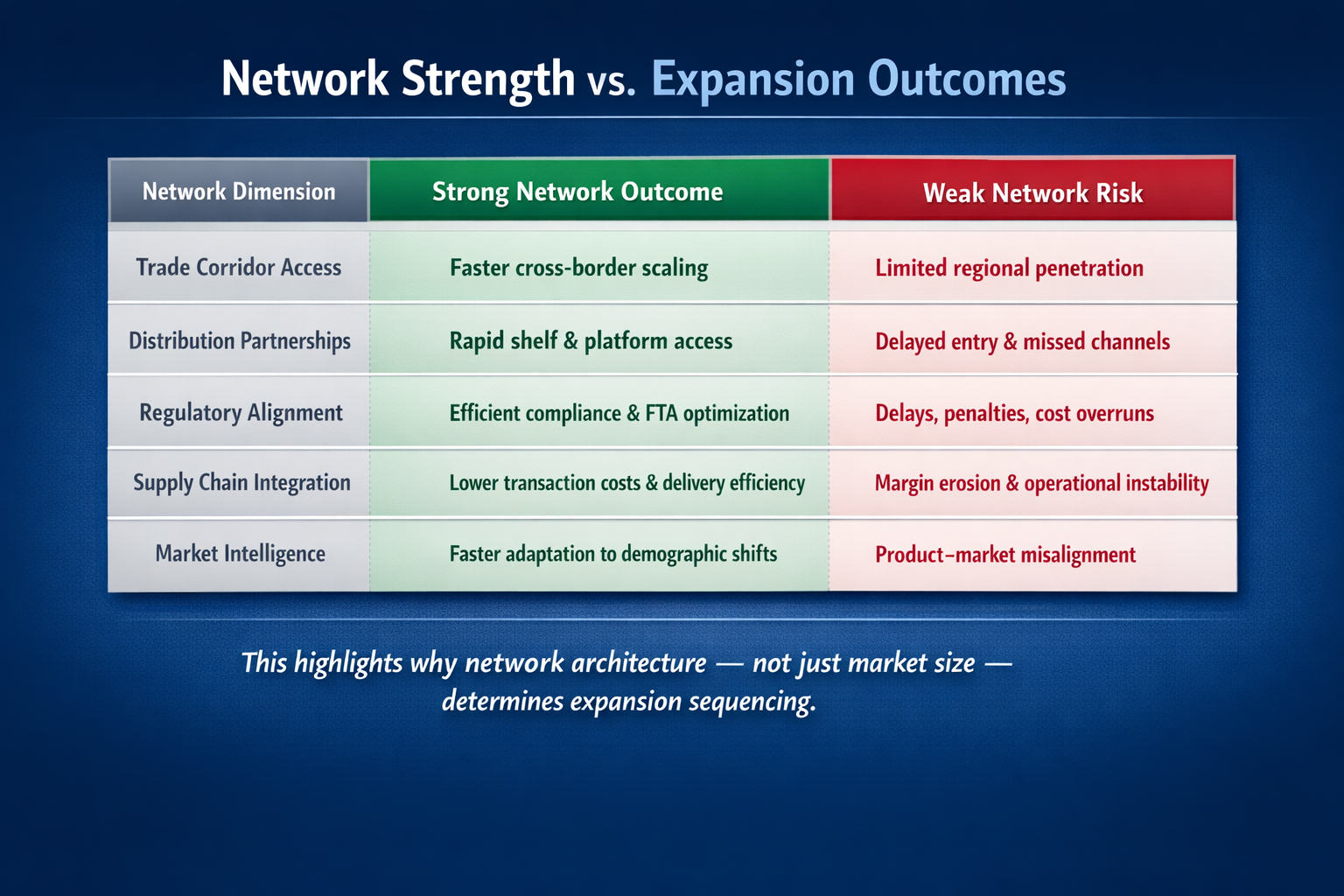

The Asia Network Readiness Framework™

Before expanding or scaling in Asia, leadership teams should evaluate their network architecture across five structural dimensions:

1. Trade Corridor Alignment

Are we positioned within high-growth intra-Asia trade lanes, particularly China–ASEAN?

2. Distribution Depth

Do our partners provide access across modern retail, traditional trade, and e-commerce ecosystems?

3. Regulatory & FTA Leverage

Are we fully utilizing regional agreements to reduce friction and optimize cost?

4. Supply Chain Integration

Are logistics relationships diversified and resilient against disruption?

5. Market Intelligence Access

Do we have embedded insight into demographic shifts and consumer behavior?

If more than one of these dimensions is structurally weak, expansion risk rises materially.

In Practice

Companies that deliberately invest in cross-border relationship-building consistently outperform transactional entrants.

We observe firms leveraging regional partnerships to:

Adapt packaging for single-household markets in South Korea

Optimize logistics routes between China and ASEAN hubs

Integrate digital commerce platforms into traditional retail distribution

Conversely, companies entering without robust network architecture often face customs delays, regulatory friction, higher logistics costs, and slower market penetration — even when demand fundamentals are strong.

The differentiator is rarely product quality.

It is network density and alignment.

Closing

Asia remains one of the most dynamic trade regions globally. Production networks are deepening. Consumer markets are evolving. Trade agreements are lowering friction. Digital channels are accelerating change.

The strategic question for leaders is not whether you have networks.

It is whether your network architecture reflects the realities of today’s trade system.

At Samana Advisory, we work with leadership teams to audit and redesign cross-border network architecture before market entry or scale expansion.

Future issues of Samana Insights will include extended frameworks and structured execution tools available to registered members.